A company’s shareholder loan is often a source of confusion, my hope is that this article will help provide clarity surrounding the mechanics of the shareholder loan as well as how it can impact guideline income in the context of a matrimonial breakdown.

A company’s shareholder loan simply represents money that has been loaned to the shareholder (displayed as a debit / asset in the shareholder loan account) or loaned from the shareholder (displayed as a credit / liability in the shareholder loan account).

Why the shareholder loan is of significance is that it is often used as a source of personal funds for the shareholder(s) to draw upon in lieu of a regular salary, particularly among small businesses. Instead of receiving a salary, the shareholder simply transfers funds from the corporation to their personal bank account and/or purchases personal items with corporate funds.

Shareholder loan transactions are shown in a company’s general ledger and the sum of these transactions, as at a point in time, are displayed on the company’s balance sheet as either a liability (representing how much is lent by the shareholder) or an asset (representing how much has been lent to the shareholder).

A credit balance in a company’s shareholder loan account (i.e. the company owes money to the shareholder) represents after-tax funds loaned to the company that can be removed tax free from the company and as such these funds will not be reflected on the shareholder’s personal tax return.

A debit balance in the company’s shareholder loan account (i.e. the shareholder owes money to the company) is required by CRA to be brought back to a credit balance within one fiscal year otherwise it is to be included as income on the shareholder’s personal tax return in the year in which it was received. Therefore, a debit balance would generally trigger a dividend and/or salary to the respective shareholder by the subsequent fiscal year. Said dividend or salary would be included as income in the shareholder’s personal tax return in the year in which it was declared.

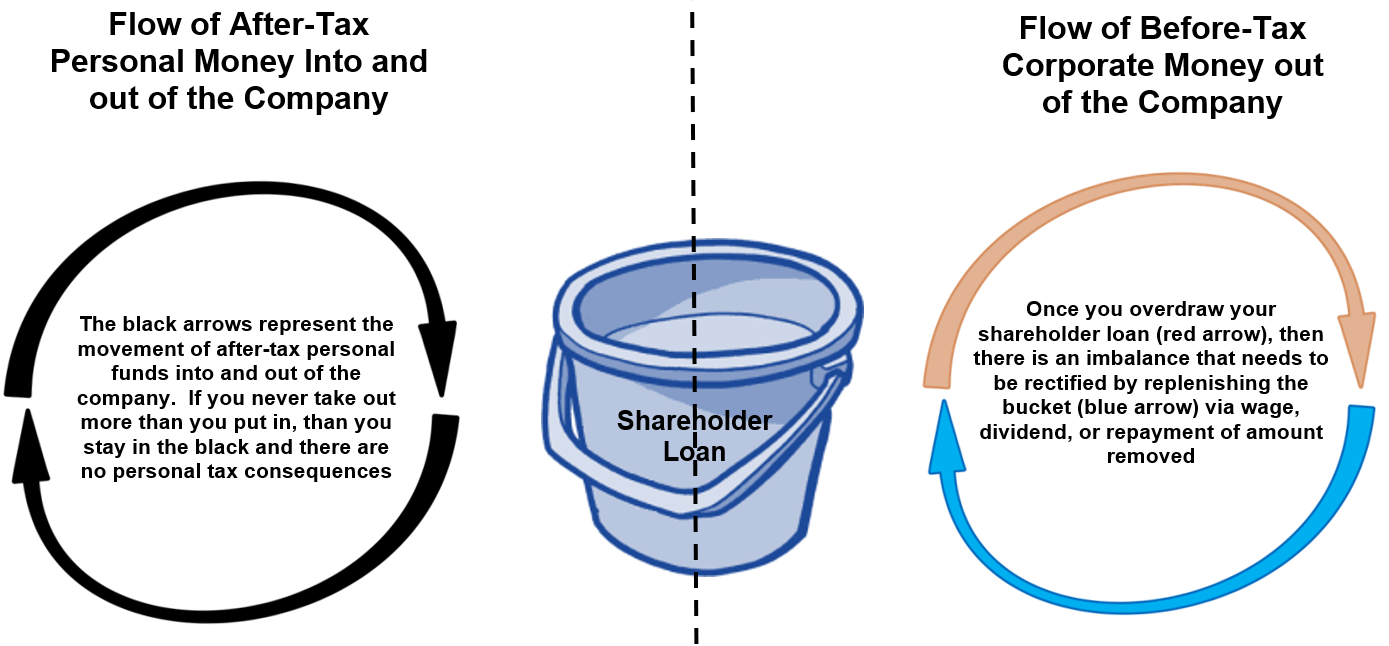

Think of the shareholder loan as a "bucket", you can only take out as much as you put in. As soon as you take out more than you’ve put in, personal taxes will be triggered via dividend and/or salary. This "bucket" analogy with regards to the shareholder loan can be illustrated as follows:

However, it is important to note that our tax system operates on the self-assessment principle which effectively means the “honor system”, in that CRA relies on the company and shareholders to properly report the shareholder loan and, where it is offside, to correct for this via a dividend and/or salary. Otherwise, the shareholder is required to include an income inclusion on their personal tax return in the year in which the funds were received.

Section 18(1) of the Federal Child Support Guidelines notes:

“Where a spouse is a shareholder, director or officer of a corporation and the court is of the opinion that the amount of the spouse’s annual income as determined under section 16 does not fairly reflect all the money available to the spouse for the payment of child support, the court may consider the situations described in section 17…”

A company’s shareholder loan may be a significant source of “money” that may not be reflected on an individual’s personal tax return, or not reflected in the applicable tax years that are being reviewed for child and/or spousal support.

As a result, when corporations are involved in matrimonial breakdowns, it is critical to review the shareholder loan detail in order to determine if it reflects a source of money that otherwise may be included (or at least considered) in guideline income.

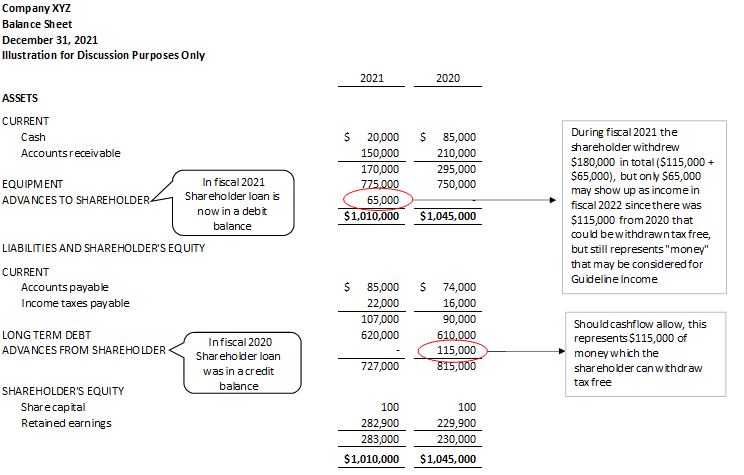

The following illustration depicts how the shareholder loan is displayed on a balance sheet as well as confusion that may result when the shareholder loan goes from a credit in one fiscal year to a debit in the next.

It is important to note that matters are always fact specific and there is not a one size fits all solution, but shareholder loan activity should be one of the factors to consider in the determination of guideline income.